Some cities faced with sluggish population growth are making an enticing offer to consumers: They’ll pay new residents—up to $10,000 in some cases—to make the city their new home. Such incentives are growing more common, according to a new report from Livability. The various metros are hoping to attract new residents to relocate and help them revitalize their economies.Cities are coming with abundant offers too, from paying off student loa

Apparently the magic number for first-time home buyers is 28. That’s the average age that most Americans think a person should be when they buy their own home, according to a new Bankrate.com report conducted last month among a sample of 1,001 respondents.This may be a bit optimistic in practice, at least for buyers in today’s market. The National Association of REALTORS®’ 2017 Profile of Home Buyers and Sellers found the median age of

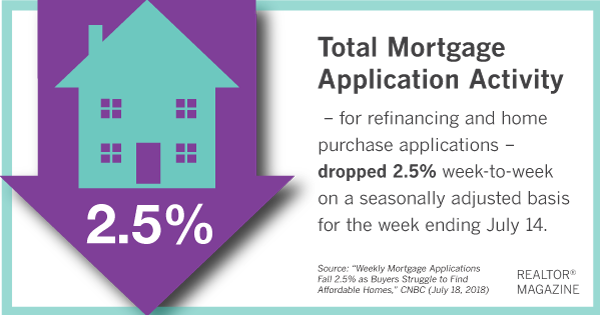

Buyer demand may be high but tight inventory is keeping that demand from translating into sales. And with fewer choices of homes for sale, some buyers are retreating. Mortgage applications fell again last week, dropping 2.5 percent on a seasonally adjusted basis, the Mortgage Bankers Association reported Wednesday. Total volume is now 12 percent lower than the same week a year ago.Home buyers were the ones who most receded from mortgage applicati

Home values can drastically differ in some areas of a metro and foster an environment of housing value inequality between rich and poor.LendingTree, an online loan marketplace, recently analyzed 50 of the largest metro areas to rank cities based on its home value Gini coefficient. The Gini coefficient ranges from 0 (complete equality where every value is the same) to 1 (complete inequality where one entity has 100 percent of the value and the ot

The cost to maintain a home is something financial experts recommend budgeting for early on, in preparation for choosing which house to buy. On average, homeowners spend 1 percent of their overall home cost in maintenance every year, according to a new study by Porch.com.The upkeep costs can vary based on style, age, type, and even location of the home. The average cost to maintaining a home each year is about $16,000, according to Porch.com’

Higher mortgage rates and rising home prices are making housing more expensive for homeowners this year compared to last year. In San Jose, Calif., for example, the average homeowner is paying $500 more for monthly mortgage payments than a year ago, jumping from $4,100 to $4,600, according to a new analysis by Bloomberg.In nearly one-third of metro areas, buyers paid an average $50 hike in monthly mortgage payments in the first quarter of the yea

You’ve heard of buyer’s remorse; but without your market expertise and sales skills to back them up, sellers who choose to sell their home on their own just may experience “seller’s regret” when they see how much less they get for their properties. FSBOs earn an average of $60,000 to $90,000 less on the sale of their home than sellers who work with a real estate agent, according to the National Association of REALTORS®. Here’s the br

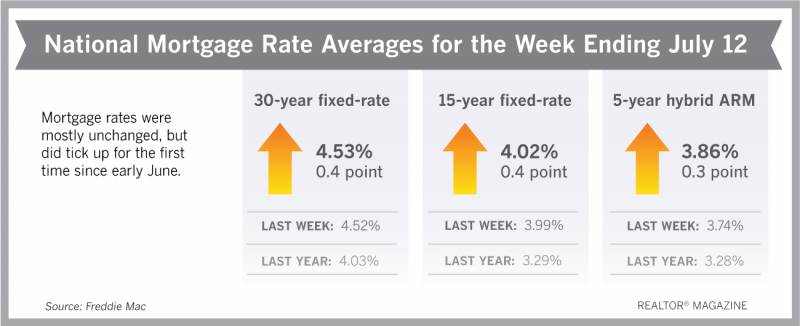

Mortgage rates were mostly in a holding pattern this week, but still eked out the first increase since early June.Overall, mortgage rates this summer have been dropping the past few weeks after sharp rises this spring. “A record number of people quit their job last month, most likely for a new opportunity with higher wages and better benefits,” says Sam Khater, Freddie Mac’s chief economist. “This positive trend, along with these lower

More luxury home sales occurred in the first half of 2018. Transactions that were $1 million–plus were up 25 percent year over year, according to realtor.com®’s Luxury Home Index. That marks the largest leap in luxury home sales since January 2014. Luxury is defined as the top 5 percent of all residential home sales in a given market.In the 91 luxury markets analyzed, the entry-level price rose 4.6 percent year over year. Seventeen of those

South Dakota is the best place to retire in 2018, according to the latest retirement rankings from Bankrate.com. South Dakotans still ranked highest for well-being, which is based on their perceptions of social, community, health, and financial security. Plus, South Dakota residents don’t have to pay income taxes when they live in the second most tax-friendly state in the country—a perk for seniors living on a fixed income.Bankrate.com accou

This website includes images sourced from third party websites including Adobe, Getty Images, and as otherwise noted.